Half the data you’re buying about golfers is wrong.

That’s not hyperbole. A Truthset study found that up to 51% of ad targeting data from third-party providers is inaccurate. Accuracy rates across major data brokers range from 32% to 69%. If you’re a golf brand spending six figures on digital campaigns, those numbers should make you uncomfortable.

The advertising industry spent the last two decades building its infrastructure on third-party cookies and purchased data segments. That infrastructure is now crumbling. And for golf advertisers specifically, the fallout is worse than for almost any other category.

Here’s why.

The Cookie Situation Is Worse Than You Think

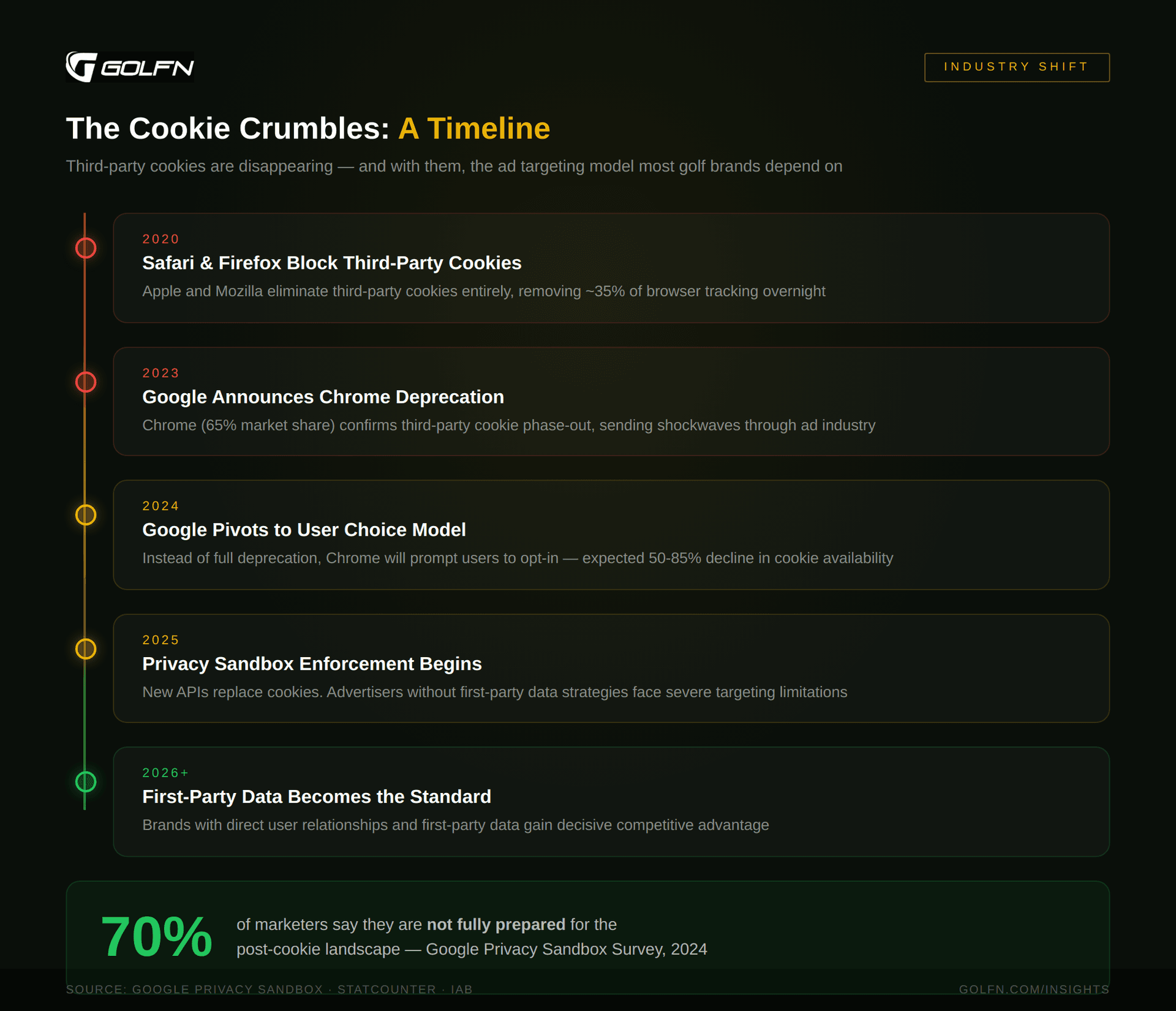

Google reversed its plan to fully deprecate third-party cookies in Chrome. In April 2025, they announced a user-choice model instead of a blanket phase-out. Some marketers took that as an all-clear signal.

It wasn’t.

Safari and Firefox already block third-party cookies by default. Together with Chrome, they cover virtually every browser in use. And when Apple launched App Tracking Transparency in 2021, only about 25% of users opted in when given a clear choice.

Google’s user-choice model will almost certainly follow the same pattern. When people are asked directly whether they want to be tracked across the internet, most say no.

A Digiday report from March 2025 found that more than 70% of digital marketers feel underprepared for the shift. Google’s own Ad Manager testing showed a 34% drop in programmatic revenue for publishers running without cookies. CPM fell 33% when advertisers relied on Privacy Sandbox alternatives.

The cookies aren’t all gone yet. But the clock is running, and the direction is clear.

Click image to enlarge

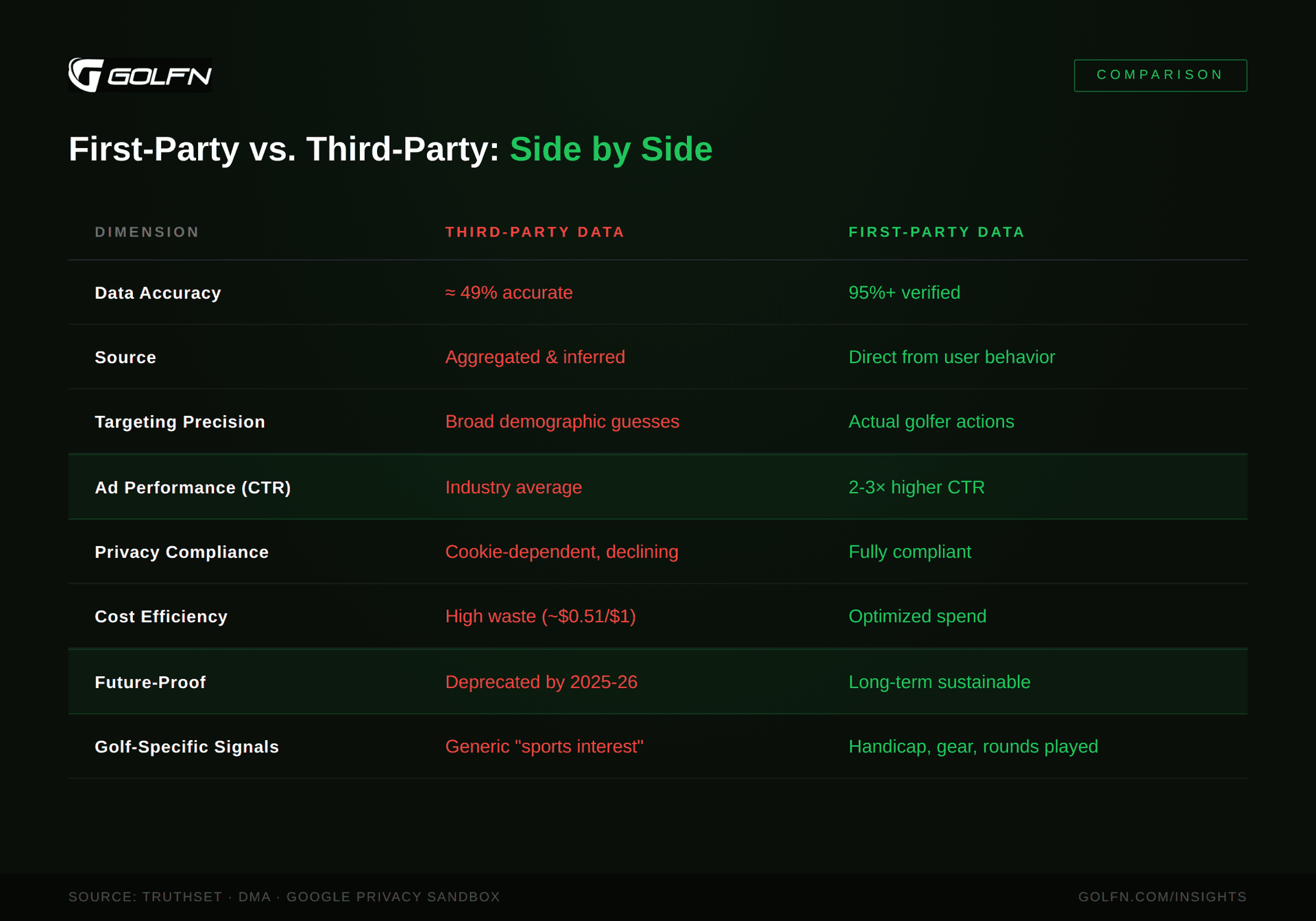

What Third-Party Data Actually Looks Like

Third-party data is collected by companies that have no direct relationship with the people in their databases. They aggregate information from public records, browser tracking, app SDKs, loyalty card programs, and dozens of other sources. Then they package it into audience segments and sell it to advertisers.

The appeal is obvious: scale. Acxiom alone claims 700 million consumer profiles with 1,500 data points each. But scale without accuracy is just expensive noise.

Here’s the problem with third-party golf data specifically.

A data broker might tag someone as a “golf enthusiast” because they visited a golf website once, watched a PGA Tour highlight on YouTube, or bought a polo shirt from a brand that also sells golf apparel. That person gets dropped into a segment called “Avid Golfers” and sold to your brand at a premium CPM.

But they might not own a single club. They might not have played a round in five years. They might not play at all.

There’s no way to verify. And that’s the fundamental issue.

Third-party data has unknown provenance. You can’t audit collection methods. You can’t verify accuracy. You can’t confirm compliance with privacy regulations. You’re trusting a broker’s word that the data represents real behavior.

Meanwhile, 30% of B2B data decays annually under normal conditions. In high-turnover categories, that number hits 70%. A 2018 Forrester study found that only 12% of marketers had high confidence in their data accuracy. 84% listed data quality as a top-five weakness.

Those numbers haven’t improved. The data sources have only gotten murkier.

Click image to enlarge

Golf Is Uniquely Vulnerable to Bad Data

Most consumer categories have broad enough audiences that some inaccuracy is tolerable. If you’re selling sneakers, a 60% accurate segment of “athletic shoe buyers” still gives you tens of millions of real prospects.

Golf doesn’t work that way.

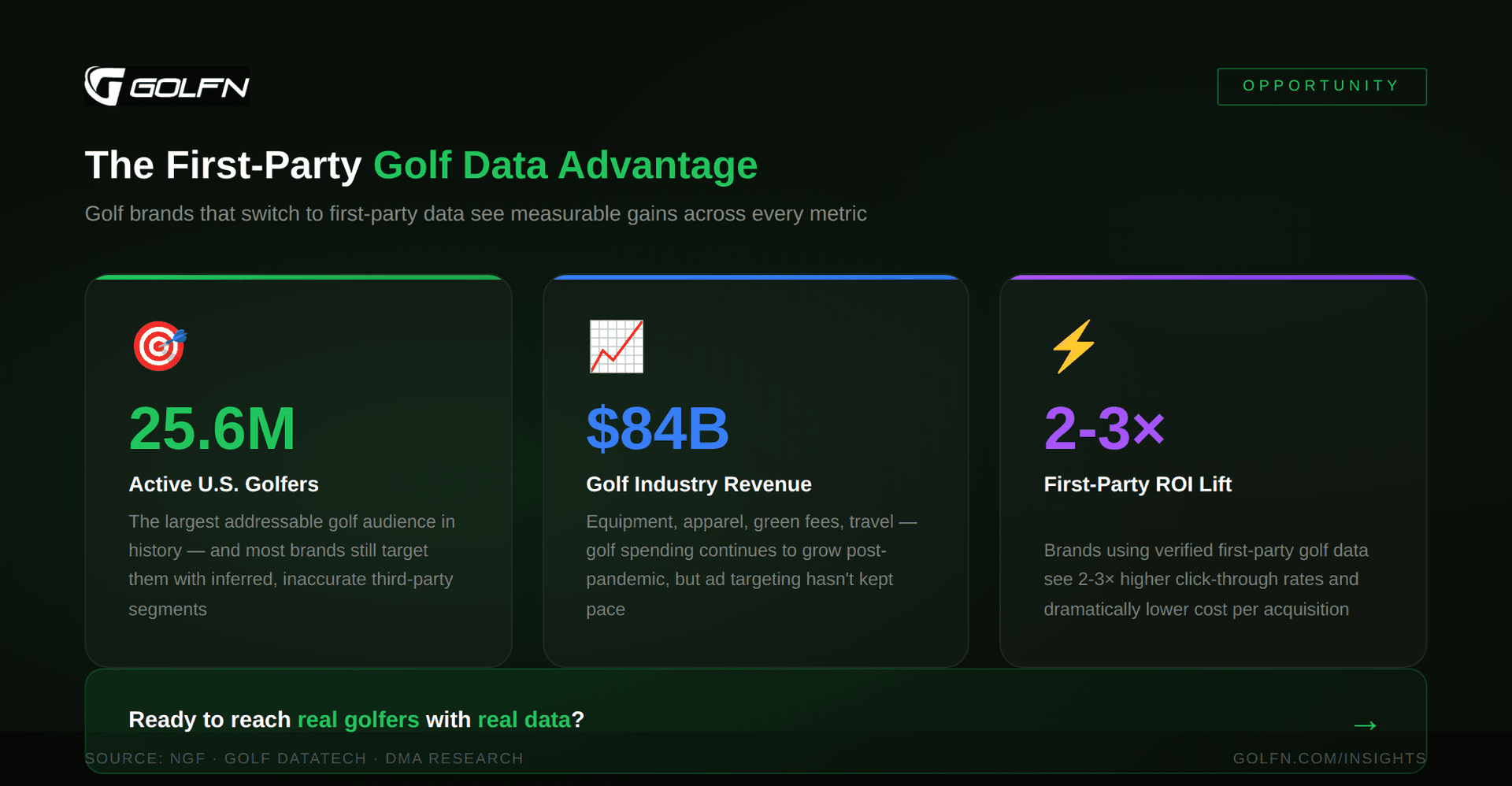

There are 45 million Americans age 6 and older who participate in golf in some form. But the people who actually buy equipment, book tee times regularly, and respond to golf advertising are a fraction of that. The addressable market for a premium driver that costs $600 is narrow. The addressable market for a $300 round at a resort course is narrower still.

When your total addressable audience is already small, data accuracy isn’t a nice-to-have. It’s the difference between a profitable campaign and a wasted one.

And golf has another problem: the demographic assumptions are almost always wrong.

The median golfer demographic is shifting fast. Women now represent 25% of U.S. golfers. The fastest-growing segment is players under 35. Yet third-party data segments still skew heavily toward the stereotype: male, 55+, household income above $150K. If your targeting relies on those inferred demographics, you’re missing a quarter of the market before you even start.

The golf equipment market hit $8.31 billion in 2024 and is projected to reach $11.64 billion by 2030. The U.S. golf apparel market alone is $2.8 billion annually. These aren’t small numbers. And the brands competing for that spend need to know that their ads are reaching people who actually play, actually buy, and are actually in the market.

Third-party segments can’t tell you that. They can only guess.

Click image to enlarge

What First-Party Golf Data Looks Like

First-party data is collected directly from users who opted in and provided it voluntarily. It’s verified at the point of collection. It doesn’t decay the same way because users update their own information as their behavior changes.

For golf, the difference is categorical.

First-party data from an engaged golfer includes their actual handicap, the courses they play, how often they play, what equipment they carry in their bag, when they last upgraded, what brands they prefer, where they live, and what they spend.

That’s not an inferred “golf enthusiast.” That’s a verified golfer with known purchase intent.

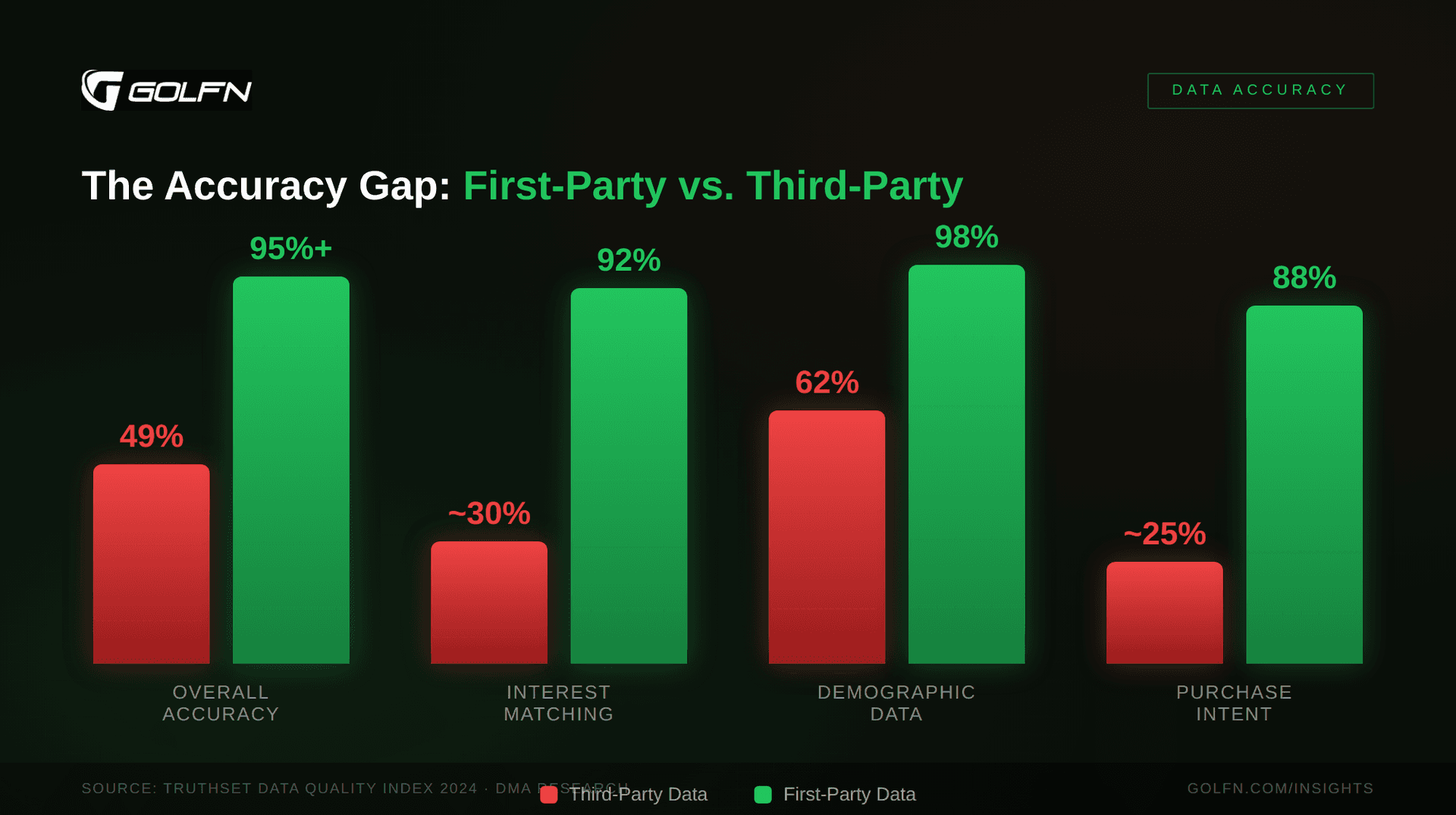

The performance difference shows up everywhere in the data. First-party checkout data improves audience match rates by 30% to 70%. Brands that unify CRM data with advertising see 30% to 50% better attribution accuracy. 90% of marketers surveyed in 2025 said first-party data improves ad performance.

The PGA Tour moved to this model. They migrated their fan data to Snowflake, implemented GrowthLoop for audience activation, and unified fan accounts, ticket purchases, and merchandise data into a single source. The result: precise segmentation without technical specialists, lower ad costs, and better performance across Meta, LinkedIn, The Trade Desk, and Google Ads.

Golf club apps show the same pattern on a smaller scale. Click-through rates of 1.5% to 2.5% against first-party audiences, compared to the industry standard of 0.5% to 1%. Average ROI of 120% to 180% on campaigns targeting verified golfers. That’s 2x to 3x the engagement rate of standard programmatic targeting.

These aren’t marginal improvements. They’re structural advantages.

Click image to enlarge

The Accuracy Gap Is a Cost Problem

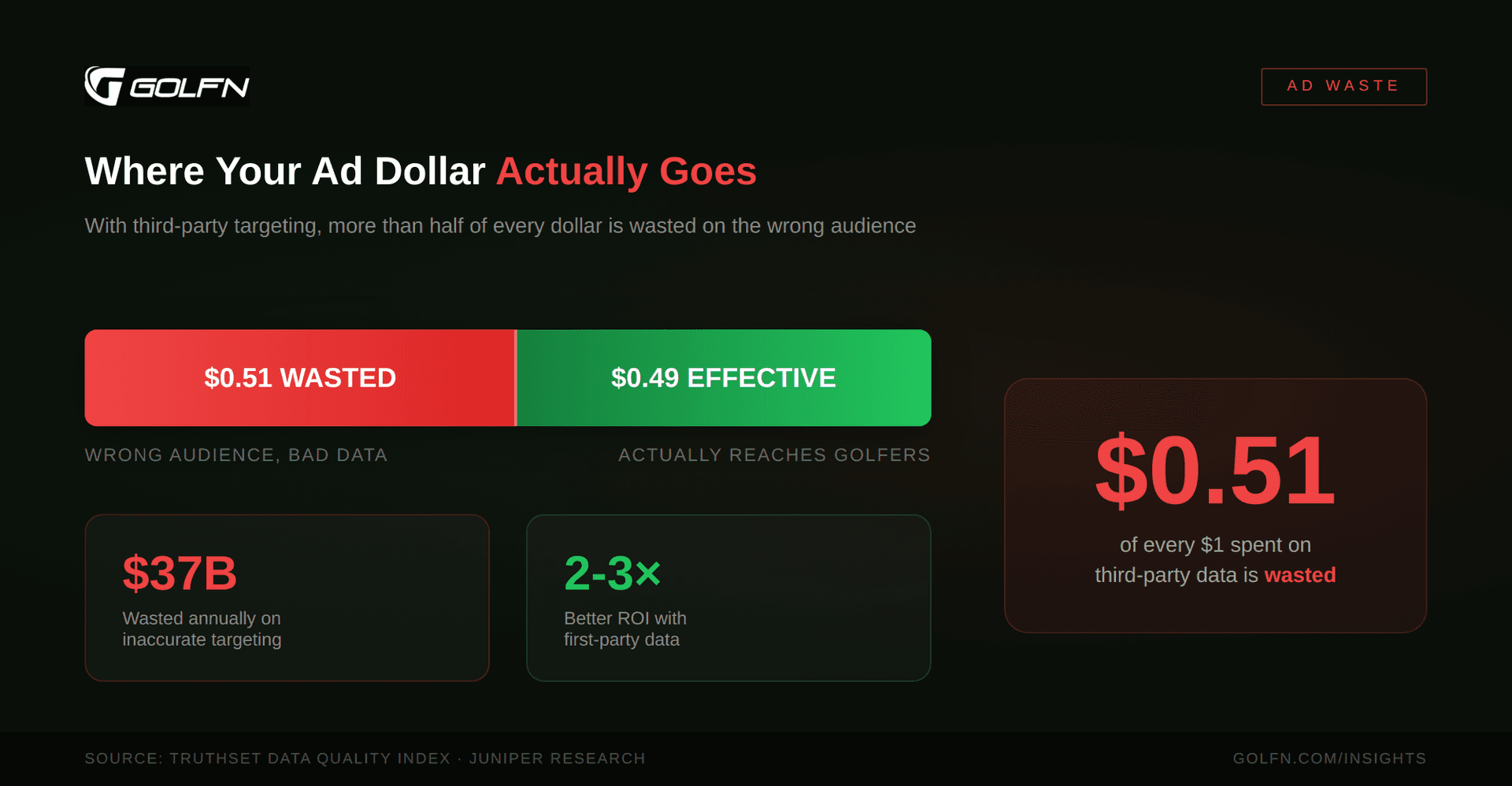

Every percentage point of data inaccuracy translates directly to waste.

If your audience segment is 50% accurate, half your impressions land on people who will never buy your product. At a $15 CPM on a $100,000 campaign, that’s $50,000 in wasted spend. Not “less efficient” spend. Wasted.

Marketing measurement studies consistently show that first-party data strategies drive 20% to 40% efficiency gains over third-party targeting. Not because the creative is better or the media mix is smarter, but because the targeting actually hits real prospects.

The math gets more extreme in golf because of the niche audience size. When you’re trying to reach the subset of golfers who are actively shopping for a new set of irons, the margin for error on targeting is nearly zero. A broad “sports enthusiast” segment from a data broker will burn through your budget before you reach 100 qualified buyers.

First-party data inverts the problem. Instead of starting with a massive pool and hoping your actual audience is somewhere in it, you start with verified golfers and build from there.

Click image to enlarge

The Competitive Disadvantage of Shared Data

Third-party data segments are available to anyone willing to pay. If you’re buying “Golf Equipment Buyers 25-54 HHI $100K+” from a data broker, so is every one of your competitors. You’re all bidding on the same audience in the same auction, driving up costs and diluting performance.

First-party data is exclusive by definition.

A brand that partners with a first-party data source owns the relationship with that audience. The segments are not available on the open market. The insights are not shared with competitors. The targeting intelligence compounds over time as the dataset grows.

In programmatic advertising, this is becoming the dividing line between brands that can afford to compete and brands that can’t. Private Marketplaces and Curated Marketplaces are emerging specifically to let publishers with strong first-party data sell access at a premium. The value isn’t just better targeting. It’s targeting that your competitors can’t replicate.

Privacy Compliance Is Not Optional

GDPR. CCPA. Virginia’s CDPA. Colorado Privacy Act. Connecticut Data Privacy Act. The list grows every year.

Third-party data has a compliance problem that most marketers ignore until it’s too late. When data passes through multiple brokers and aggregators, the chain of consent becomes impossible to trace. Did the original user actually opt in? Under what terms? Was the data collected in a jurisdiction covered by privacy law? Was it shared in compliance with those laws?

Most brands can’t answer those questions about their third-party data. And regulators are starting to notice.

First-party data collected with explicit opt-in consent is inherently compliant. The user provided their information directly. The terms of collection are documented. There is no chain-of-custody question because there is no chain.

For golf brands marketing to an affluent, privacy-conscious demographic, this matters. The same audience that has disposable income for premium equipment is also the audience most likely to use ad blockers, opt out of tracking, and pay attention to how their data is used.

71% of publishers now recognize first-party data as the key source of positive advertising results. 85% expect its role to increase in 2026. The industry isn’t debating whether the shift will happen. It’s debating how fast.

What This Means for Golf Advertisers

The golf advertising market has a structural data problem. Third-party segments are too broad, too inaccurate, and too shared to serve a niche audience effectively. The cookie infrastructure that made those segments functional is eroding. Privacy regulations are tightening the screws further.

First-party data from verified golfers is the correction.

Not because privacy regulations forced it. Not because cookies disappeared overnight. But because accurate data targeting actual golfers will always outperform inferred segments targeting “people who might be golfers.”

The brands that figure this out early will spend less to reach more qualified buyers. The brands that don’t will keep pouring money into segments where half the audience doesn’t own a putter.

The data is clear. The direction is set. The only question is whether you make the shift now or after your competitors already have.

GolfN’s 50,000+ verified golfers provide opt-in first-party data including handicap, equipment, course history, and purchase behavior. If you’re a golf brand spending on digital advertising and want to see what accurate targeting looks like, reach out.