The golf consumer is not who most media plans say they are. That gap between perception and reality is where advertising budgets go to die.

This is the data. Updated for 2026, sourced from the National Golf Foundation, industry reports, and GolfN’s first-party user base. If you are a brand manager,

media buyer, or CMO trying to figure out where golf consumers actually are, how they spend, and how to reach them, start here.

The Size of the Market

Golf participation hit an all-time high in 2025. The total is 48.1 million Americans who played golf on-course or off-course, a record. That number is up 50% over the past decade.

On-course participation reached 29.1 million, the eighth consecutive year of growth and the highest number since the Tiger Woods peak in 2003. Off-course participation (driving ranges, simulators, entertainment venues like Topgolf) reached 37.9 million, with 19 million playing exclusively off-course.

Rounds played at U.S. courses set another all-time record in 2025, the fourth time in five years. For the sixth consecutive year, Americans played more than 500 million rounds nationally. That streak is unmatched in the history of the sport.

Here is the part that matters most for advertisers: this is happening with roughly 2,000 fewer golf courses than existed during the early-2000s peak. There are approximately 15,900 courses at nearly 14,000 facilities in the U.S. today. Demand is rising while supply contracts. That means more concentrated, more engaged consumers at every facility.

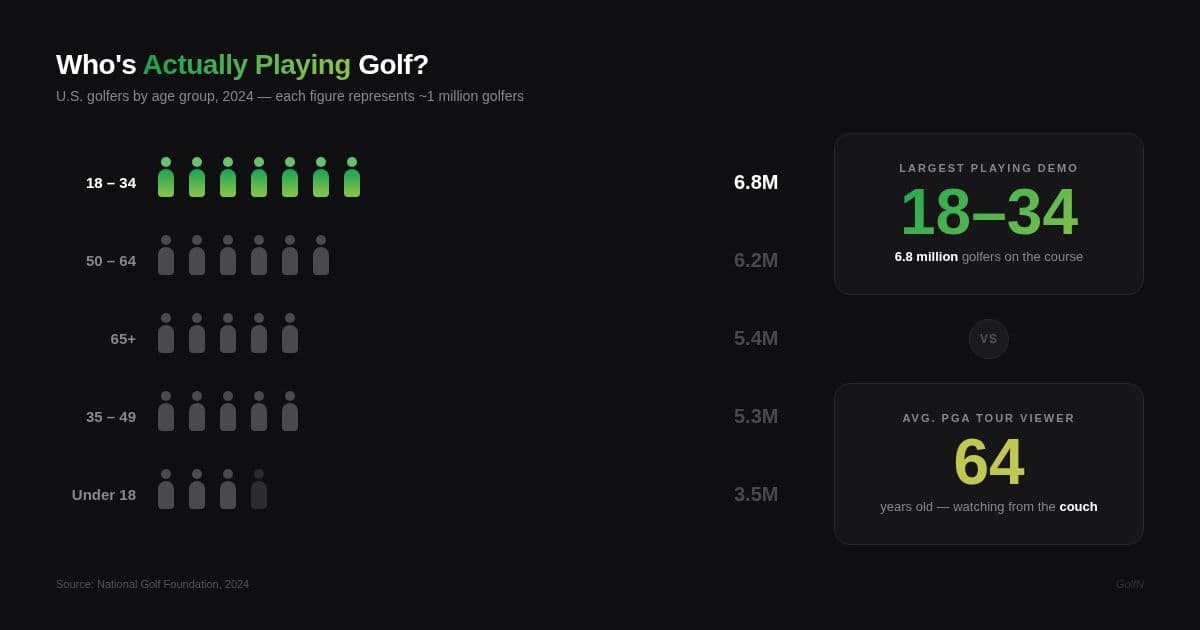

Age: The Biggest Misconception in Golf Marketing

The average PGA Tour broadcast viewer is 64 years old. That number has defined how golf advertising gets bought for decades. It should not.

The largest on-course age group in the U.S. is 18 to 34. In 2024, 6.8 million golfers fell in that bracket, more than any other demographic. The 50-to-64 group came in second at 6.2 million.

Read that again. The youngest adult cohort is the biggest.

Click image to enlarge

Over 7 million young adults have only hit golf balls off-course so far, creating a pipeline of future on-course golfers. Another 7.5 million non-golfers aged 18 to 34 say they are “very interested” in playing.

74% of golfers aged 18 to 34 plan to purchase a membership or season pass at a golf facility. That is higher than any other age group. These are not casual dabblers. They are committed players with buying intent.

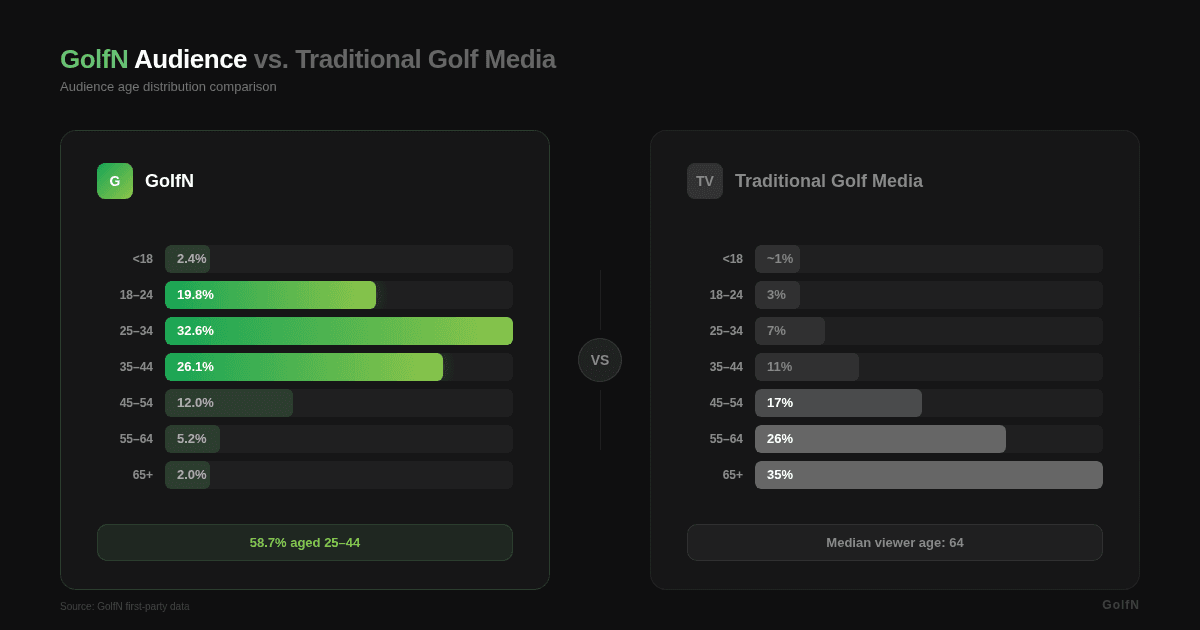

GolfN’s user base reflects this shift. 59% of GolfN users are between 25 and 44. That is not a coincidence. It is where the sport is going, and the data confirms it.

If your media plan is built around Golf Channel and print, you are buying access to the 64-year-old viewer. The 28-year-old who plays three times a month and buys gear on his phone is somewhere else entirely.

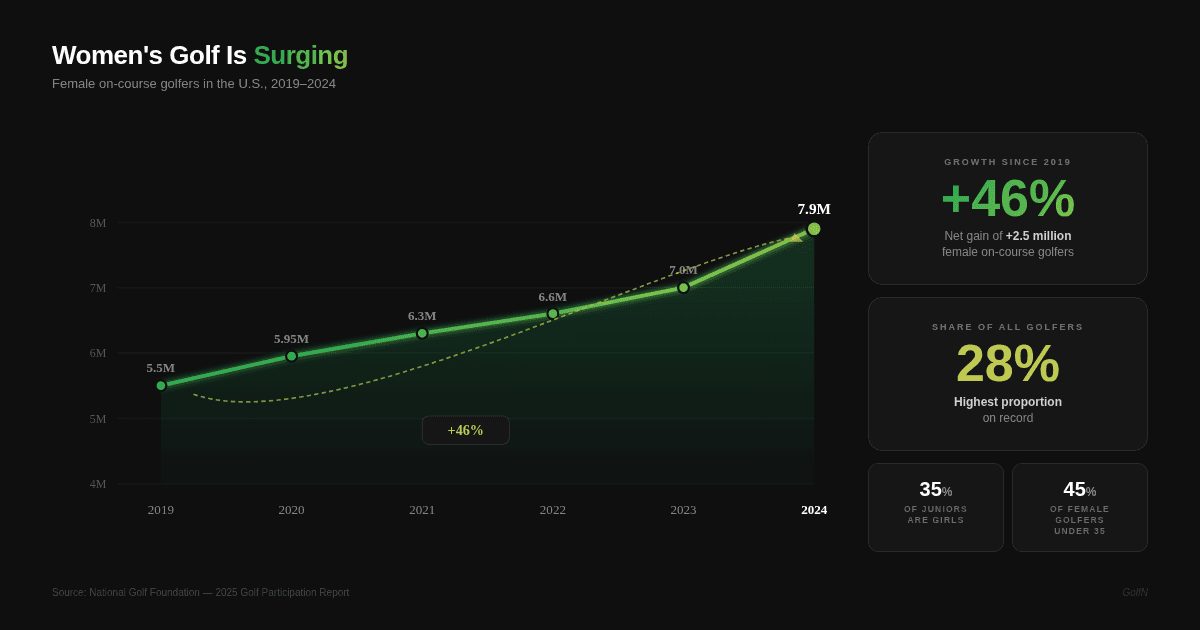

Women’s golf participation hit an all-time high in 2025. Over 8 million women and girls played on-course, a 46% increase since 2019.

Women now represent 28% of on-course golfers, the highest proportion on record. They represent an even larger share of beginners (35%), juniors (35%), and off-course-only participants (43%).

This is not a niche segment. This is a structural shift in who plays golf.

Click image to enlarge

Women’s golf equipment sales rose 22% in recent years. Women’s apparel is growing faster than the overall golf apparel market. Brands that treat women golfers as an afterthought are ignoring one of the fastest-growing consumer segments in the sport.

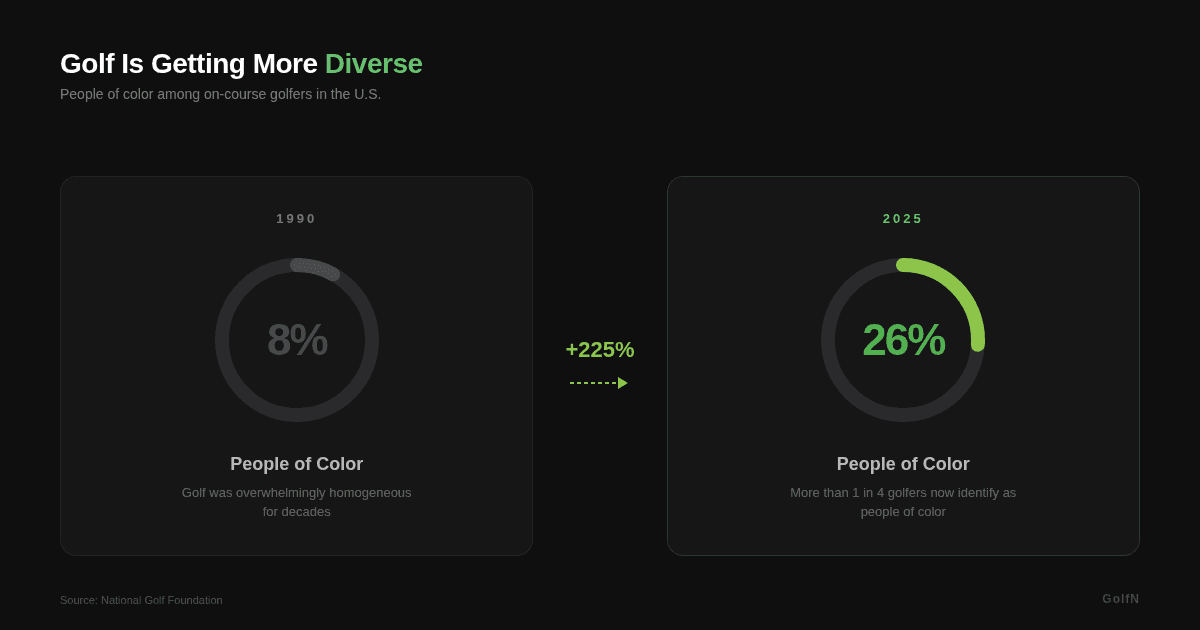

Diversity: The New Composition

26% of on-course golfers in 2025 were Black, Asian, or Hispanic, the highest ever recorded and up from 25% the year prior. That is roughly 7.5 million people, compared to 8% representation in 1990.

Click image to enlarge

Junior golf is leading this shift. Just under 4 million juniors played on a course in 2025, a 58% increase since 2019, the largest gains of any age group. 26% of junior golfers are people of color, compared to 6% just twenty years ago. 35% of junior golfers are girls. The pipeline of future adult golfers looks fundamentally different from the current base.

Off-course participation is even more diverse. 45% of off-course-only golfers are people of color. 43% are women.

Any brand building a long-term golf marketing strategy needs to account for this reality. The golfer of 2030 is already in the system. The demographic data tells you exactly what they look like.

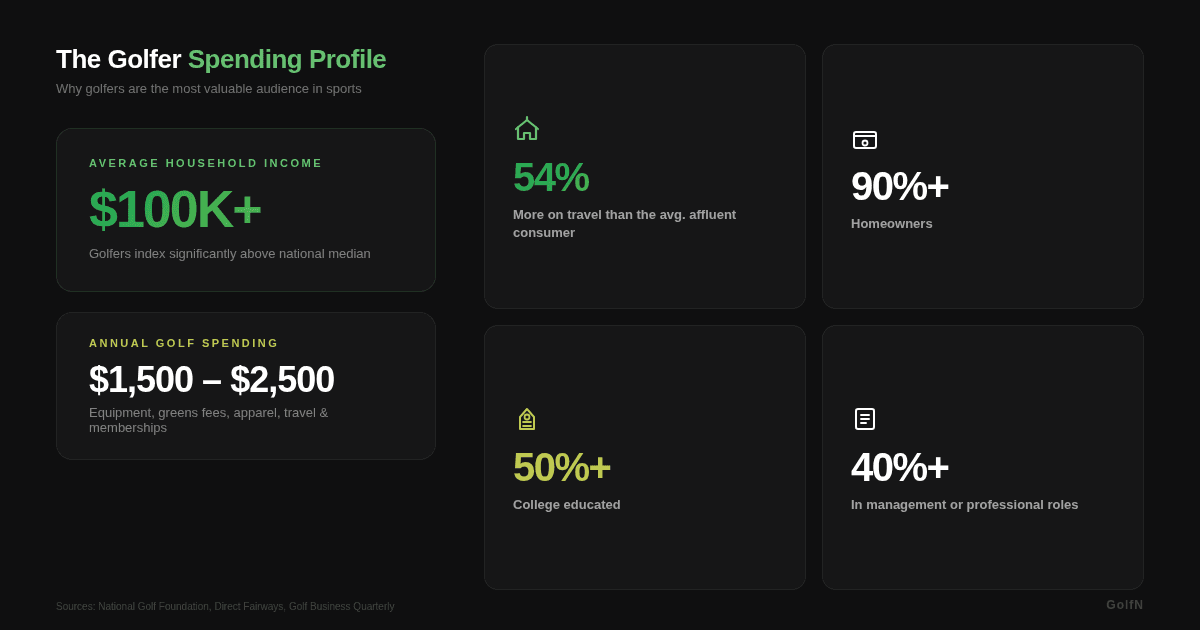

Income and Spending Power

Golfers are affluent consumers. The average household income of regular golfers exceeds $100,000. Most golfers come from households earning $75,000 or more, with roughly a quarter reporting household incomes above $300,000.

Over half of golfers who regularly practice hold a college degree. Over 40% are in management positions. Over 90% are homeowners. These are high-earning, high-spending consumers with disposable income and brand loyalty.

Click image to enlarge

Annual golfer spending on golf-related activities (green fees, equipment, memberships, travel) ranges from $1,500 to $2,500 per year on average. Avid golfers spend significantly more. Golfers spend 54% more on travel than the average affluent consumer.

The spending extends well beyond the course. Golfers are disproportionately active consumers of financial services, luxury goods, automotive, travel, real estate, and technology. A brand that reaches a verified golfer is reaching an above-average consumer across nearly every spending category.

Equipment Market

The global golf equipment market is valued in the range of $9 billion to $17 billion in 2025, depending on how broadly “equipment” is defined (clubs and balls only versus clubs, balls, bags, shoes, and accessories). North America accounts for roughly 40% to 55% of global revenue.

Golf clubs remain the largest product segment, accounting for approximately 39% to 45% of equipment revenue. Golf balls follow, then bags, shoes, and accessories. Apparel is the fastest-growing segment.

The golf apparel market alone is estimated between $4.5 billion and $9.5 billion globally in 2025, growing at 5% to 7% annually. North America holds the largest share. The growth is driven by younger and female golfers who treat golf apparel as crossover lifestyle wear, not just course clothing.

Smart golf equipment (wearables, launch monitors, simulators) generated over $1 billion in recent revenue. 25% of golfers under 30 use wearable tech for training. Golf simulator sales have grown over 35% in recent years. Technology adoption is concentrated in the younger demographic.

Brand loyalty in golf is high. Titleist, Callaway, and TaylorMade dominate equipment. Peter Millar and Adidas lead men’s apparel. Over 40% of equipment purchases are influenced by professional endorsements. Customized club orders are increasing rapidly as younger golfers demand personalized gear.

Where Golf Consumers Spend Their Attention

This is the data point that should change how you allocate budget.

Golfers under 40 consume golf content on YouTube, Instagram, and TikTok. Not Golf Channel. Not magazines. The shift is not subtle. It is a generational migration that has already happened.

98% of golfers surveyed say they watch professional golf on television. But the viewership demographics of those broadcasts skew dramatically older. The golfer who watches the Masters on Sunday and the golfer who buys gear on Monday morning are increasingly different people reached through different channels.

Over a third of golfers book tee times online, with 57% of those using smartphones. Digital-first behavior is the default for younger golfers. They discover brands through social content, make purchase decisions through creator recommendations, and complete transactions on their phones.

50% of golfers aged 18 to 34 say they would consider replacing traditional golf outings with visits to entertainment venues like Topgolf and indoor simulators. This is not a threat to the sport. It is an expansion of where golf consumers spend time and money.

Golf apps are where the most engaged golfers interact with the sport daily. Score tracking, GPS, handicap management, rewards. A golfer who opens an app before, during, and after every round is the highest-value touchpoint in the entire golf consumer landscape. That is verified, active, behavioral data. Not a modeled audience segment.

One more number worth knowing: roughly two-thirds of green-grass beginners now enter the game with off-course experience. Topgolf, simulators, and tech-enabled ranges are the new front door to on-course golf. Brands that only advertise on the course are missing the pipeline entirely.

The Spending Profile Brands Should Actually Target

Here is what the data adds up to.

The golf consumer in 2026 is younger than the industry narrative suggests. Higher-spending than most media buyers assume. More diverse than five years ago. More digitally active than traditional golf media can reach. And increasingly engaged through apps, social content, and off-course venues.

The gap between this reality and how most golf advertising dollars get allocated is enormous. Tournament sponsorships and broadcast buys still dominate budgets despite reaching an audience that is older, harder to measure, and increasingly disconnected from the consumer most brands say they want.

The brands that win in this market will be the ones that start with the data, not the tradition. For a full breakdown of channels and strategies, see our guide: How to Advertise to Golfers in 2026.

GolfN Audience: A First-Party View

GolfN’s verified user base provides a direct window into the active golf consumer.

59% of GolfN users are between 25 and 44 years old. That age concentration is the inverse of traditional golf media audiences. Every user is verified through app activity. Rounds are logged. Equipment preferences are declared. Geographic behavior is observed from actual play.

Click image to enlarge

GolfN users are active golfers who track scores, manage handicaps, and engage with the app before and after every round. That behavioral data creates targeting precision that no third-party segment or broadcast buy can match.

For brands looking to reach the golf consumer described in this report, the first question to answer is simple: can you verify your audience? If the data says yes, the rest of the strategy follows.

GolfN provides brands with access to verified, first-party golf consumer data for targeted advertising campaigns. To learn how GolfN’s audience data can inform your golf marketing strategy, request a demo.

![Golf Consumer Demographics & Spending Data [2026]](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fe3wja34v%2Fproduction%2F2f0378060d26542aba71d5796c46e1638c2769f3-1200x630.png&w=3840&q=75)