Insights5 min read

Golf Sponsorship vs Golf Advertising: What Brands Should Buy

Sponsorship and advertising solve different problems in golf. A decision matrix for CMOs and partnership leads on what to buy, when, and how to measure it.

![Golf Media Buying Guide [2026]: Where Brand Dollars Actually Work](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fe3wja34v%2Fproduction%2Fc3e8984bdba3182a22f80185094f667398c35696-1200x630.png&w=3840&q=75)

Learn how GolfN can connect your brand with golf's most engaged audiences.

Explore Advertising →Golf media buying in 2026 is not "buy Golf Channel and hope." The people playing the game are younger and more fragmented than the people watching it on TV. Smart plans put money where verified golfers actually are: first-party apps, creators, search, selective streaming. Then, and only then, prestige inventory. Measure by verified reach and real actions. Not logo screenshots.

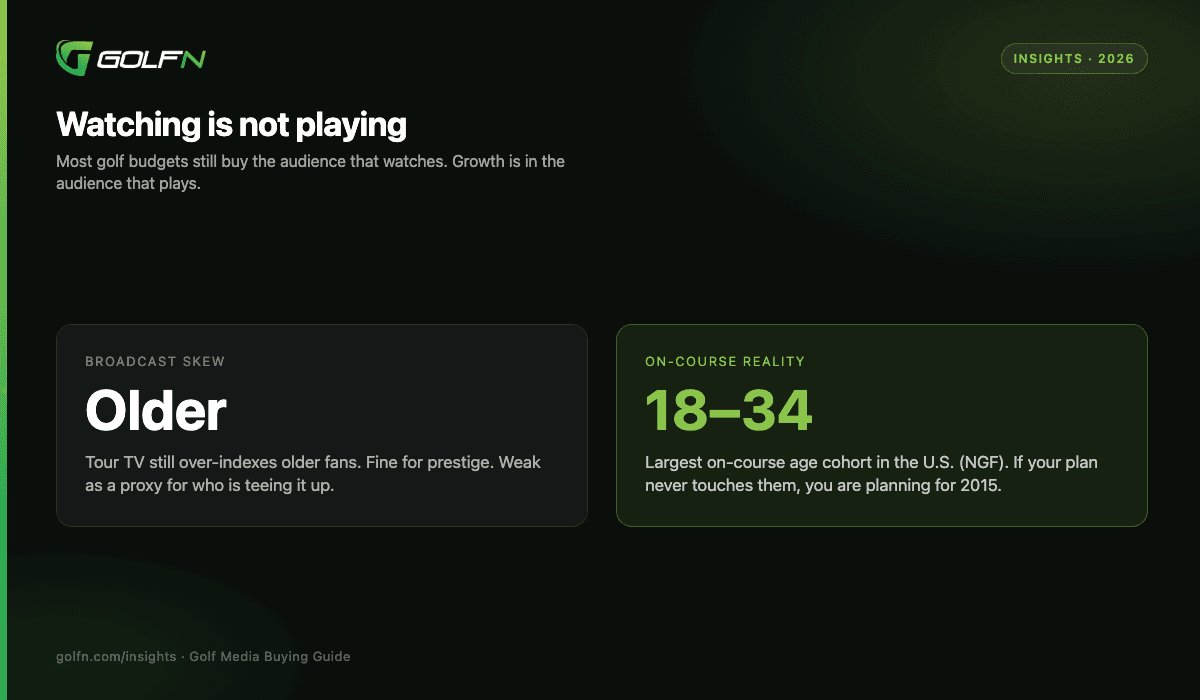

Most golf budgets still fund the watching audience.

Growth lives in the playing audience.

Those are not the same people. Broadcast golf still skews old. On-course participation does not. Adults 18 to 34 are now the largest on-course cohort in the U.S. That is not a forecast. It is the NGF's picture of who is actually teeing it up.

If your plan starts with "we need a presence around the Tour" and never asks "can we prove we reached golfers who play," you are buying brand theater. Sometimes that is intentional. Most of the time it is habit.

This guide is the money map. Where the dollars should go, what each channel is good for, and how to stop paying for golf enthusiasts who have never held a club.

For the market context behind these shifts, read The State of Golf Marketing 2026. For the philosophy of verified spend, read How to Advertise to Golfers in 2026.

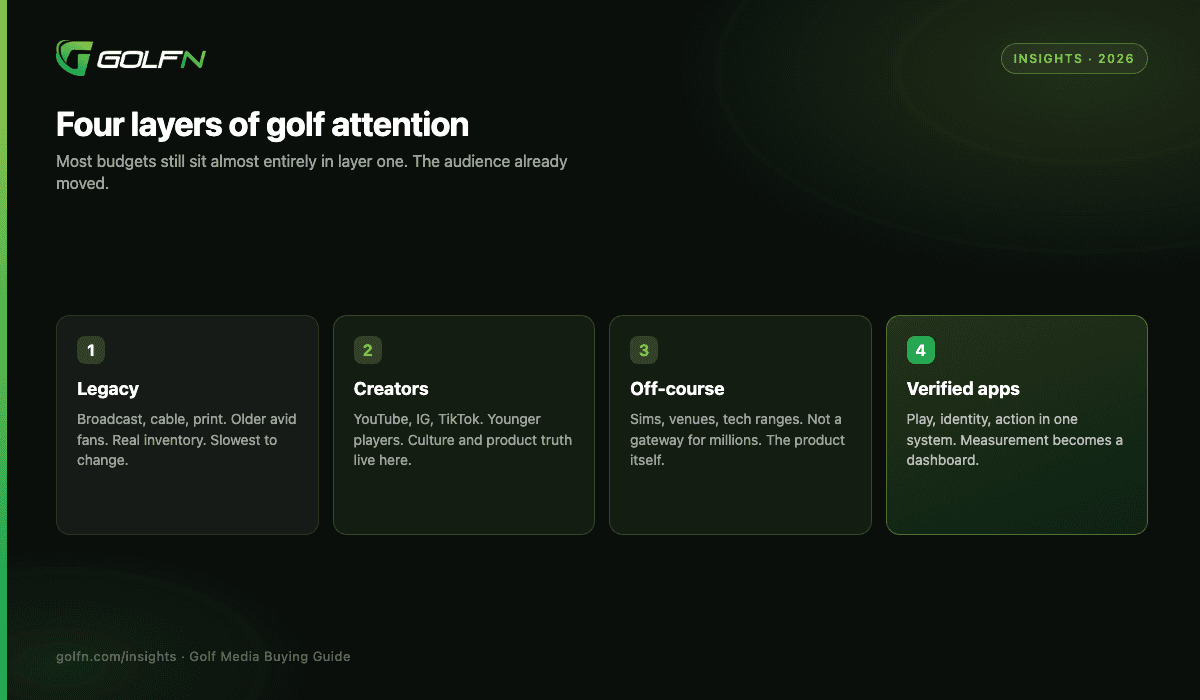

Attention in golf is not one pile. It is four layers. Most budgets still sit almost entirely in the first.

Golf Channel. Network windows. Magazines. This is where older, high-affinity fans still gather. It is real inventory. It is also the layer that moved slowest while the rest of the map changed.

YouTube. Instagram. TikTok. Golf creators with real communities, commerce, and events. Younger players live here. Capital markets already treat the top creators like media companies. Your plan should too.

Simulators. Entertainment venues. Tech ranges. For millions of people, this is not a gateway to "real golf." It is the product. Ignore it and you ignore growth.

Booking. Loyalty. GPS rounds. Rewards. The only layer where identity, play, and action can sit in the same system. This is where measurement stops being a story and starts being a dashboard.

If 70% of your golf budget is still layer one, you are planning for 2015.

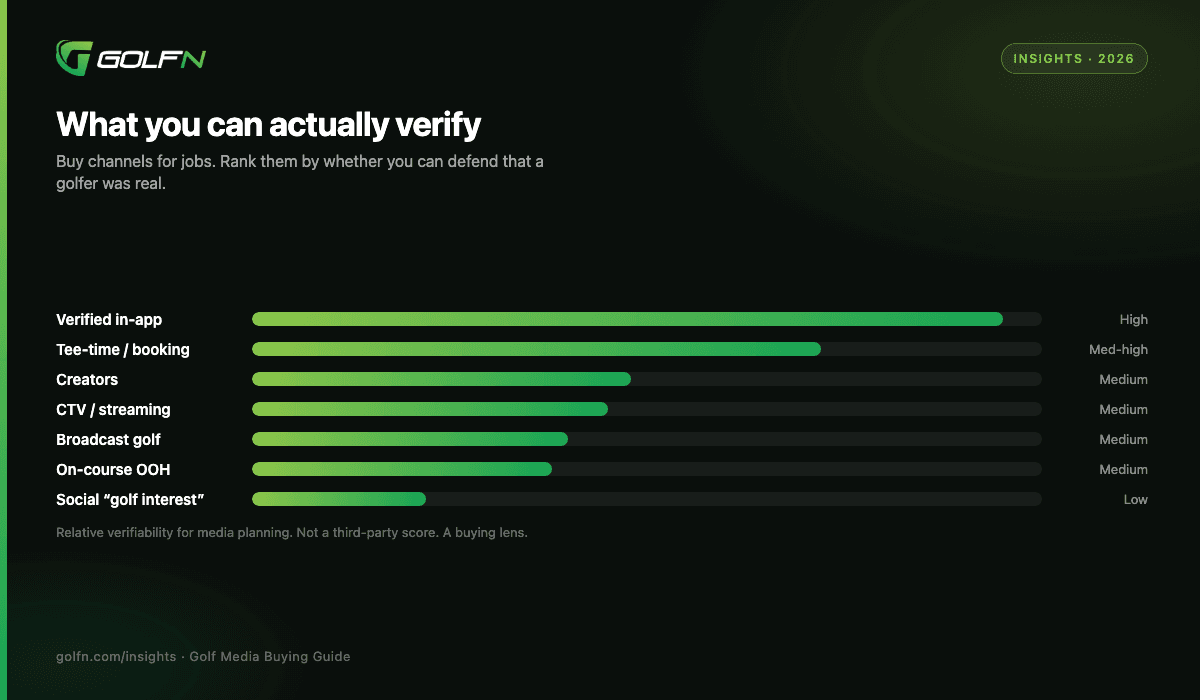

Buy channels for jobs. Not for dec decks.

Channel scorecard

| Channel | Typical age skew | Audience verifiability | Measurability | Best use | Main risk |

|---|---|---|---|---|---|

| Broadcast and cable golf | Older | Medium | Low to medium | Prestige, 55+ brand presence | Misses the growth demo |

| Streaming and CTV | Mixed | Medium | Medium | Brand with better targeting than linear | Cost and limited inventory |

| Creators (YouTube, IG, TikTok) | Younger | Medium (followers are not golfers) | Medium | Trust, culture, product truth | Fake engagement, weak tracking |

| Verified in-app platforms | Active players | High | High | Performance, rewards, offers | Scale depends on the platform |

| Tee-time and booking media | Bookers | Medium to high | Medium to high | Intent near purchase of a round | Context is price shopping |

| On-course, cart, clubhouse | Players on site | Medium | Low to medium | Local and captive attention | Hard attribution |

| Print and legacy pubs | Older avid | Medium | Low | Heritage brands | Shrinking attention share |

| Paid search and retail media | Intent-driven | Low to medium | High | Capture demand already in market | Expensive head terms |

Still works when the job is prestige and the target is older avid fans. It fails as the primary buy if you want 18 to 34 players or product action you can prove. Buy it with eyes open. Do not buy it because "that is what golf advertising is."

Better demographic control than linear. Still premium. Treat it as brand with a dashboard, not as performance media unless the partner can prove golf-qualified reach.

A mid-tier creator who plays four times a week will beat a full-page print ad with people under 40. Co-create. Do not buy a scripted product mention and call it authentic. Micro and mid-tier creators are often underpriced relative to what they move. The big names cost big money. The middle is where the math often works.

This is the only channel class that can answer a simple question: did a real golfer see this, and what did they do next?

GPS-verified rounds. Declared bags. Geo from actual play. Engagement you can report without inventing a "golf enthusiast" segment. Reward-funded formats change the game further. The ad becomes value. Gear. Entries. Access. Golfers respond to that. They do not respond to another banner on a feed they scroll past.

Strong when someone is already buying a round. Weak if you confuse a booker with a brand relationship. Use it for intent. Do not confuse it with a full funnel.

Captive. Local. Hard to attribute. Fine as a regional layer. Bad as your only "proof we were in golf."

Heritage. Slow. Older. Use when the brand story needs paper. Do not use it to hit young players.

Still one of the cleanest intent buys in the category. Someone searching "best irons 2026" is not a mystery. Pair search with verified audiences when you retarget or extend. Do not build the whole plan on generic "golf" keywords and hope.

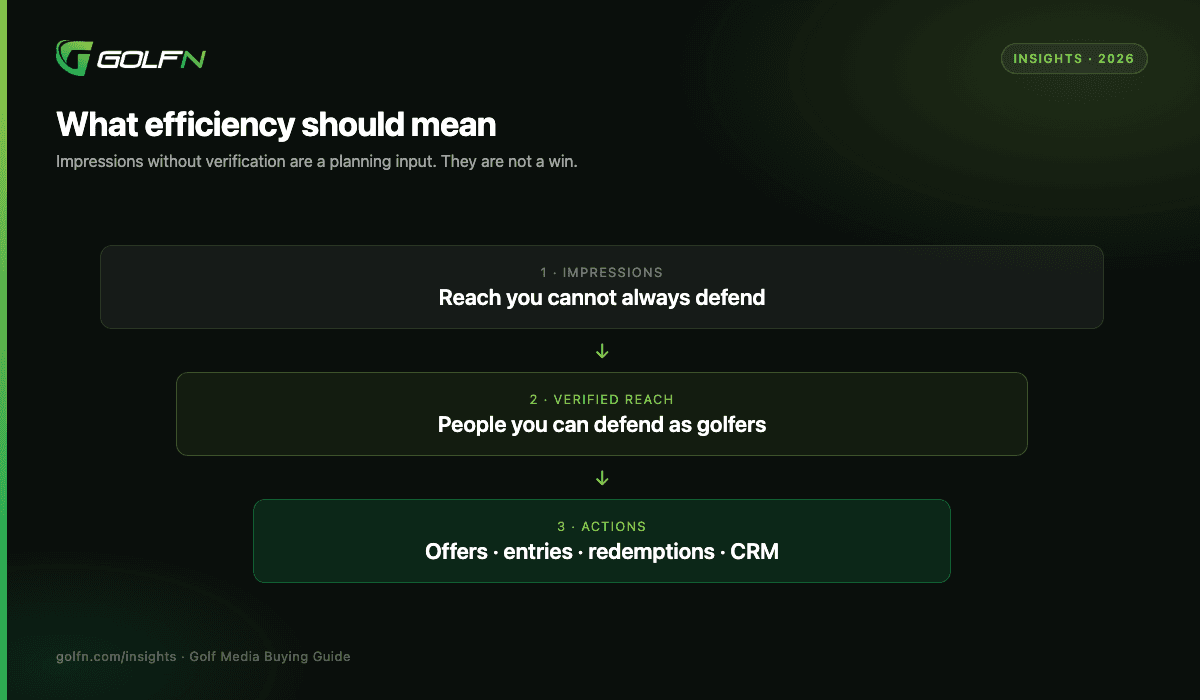

Meta ROAS copy-paste does not translate cleanly to golf.

Efficiency here means:

Impressions without verification are a planning input. They are not a win.

Cobra's marketing leadership has said the quiet part out loud on inferred audiences: a huge share of Meta "golfer" spend is waste. Every year. If your golf plan cannot beat that honesty test, it is not efficient. It is familiar.

For the full scorecard language we use internally and with partners, see Measuring Golf Marketing ROI once that piece is live. Until then, the rule is simple. Verified reach and actions first. Vanity reach last.

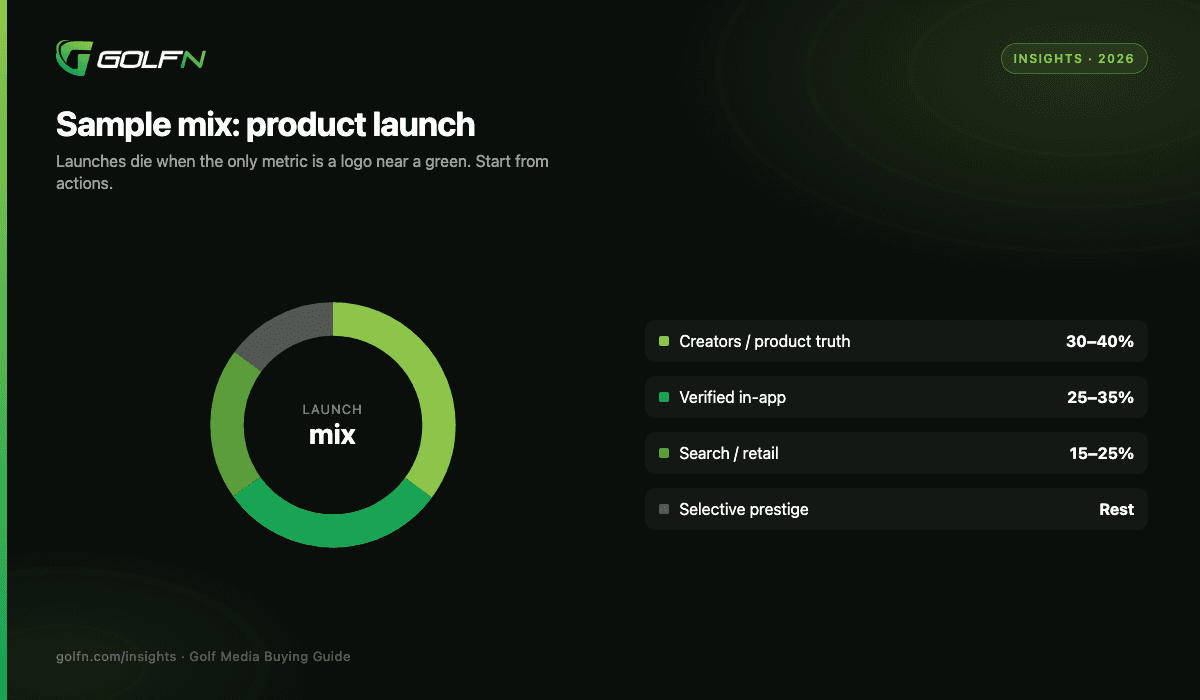

There is no universal split. There is a default that growth-oriented brands should argue from.

You are buying memory and status. Still instrument something. Unique codes. App activations. CRM. Otherwise you will never know if the prestige worked.

Launches die when the only metric is "we got a logo near a green."

If you cannot name the action, you are not running performance.

See Best Ways to Reach the 18-34 Golf Demographic.

These are starting points. Steal the logic. Adjust the weights.

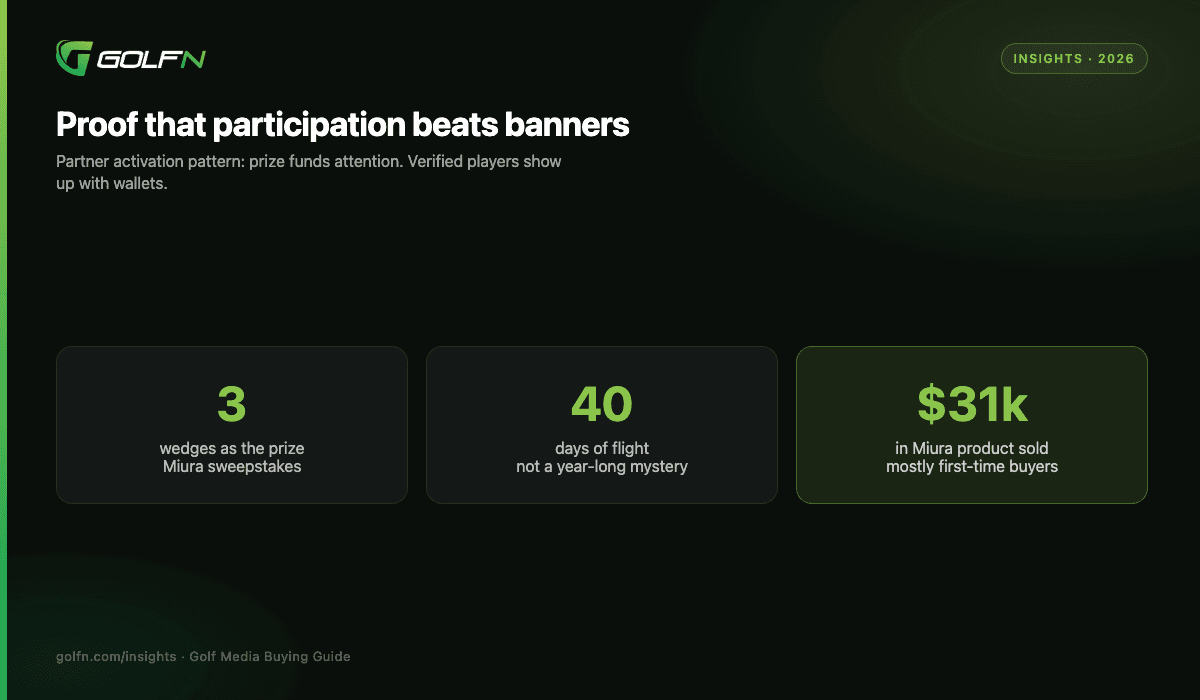

Proof that this model works in market: we ran a Miura sweepstakes with three wedges as the prize. In 40 days, GolfN users bought about $31k in Miura product. Most of them first-time Miura buyers. That is not a banner story. That is a participation story.

Golf over-indexes for premium categories. Affluence without verification is still a weak buy.

Endemic brands (equipment, apparel, soft goods) can live deeper in product and bag data. They care about MAP, dealer relationships, and who is due for a driver.

Non-endemic brands care about quality of attention and brand safety. They should demand verification harder, not softer. "We showed up at a tournament" is not a strategy. "We reached verified players in these geos who engaged with this offer" is.

If a partner cannot answer these, you are the product.

For placement-level decoding of kits and packages, see Golf Media Kit Explained when live.

We did not build another scorecard app and bolt ads on the side.

We built a first-party system around verified play. Rounds. Engagement. Rewards. Offers. In-round surfaces. Native placements golfers actually use.

What that means for a media plan:

If you want the product walkthrough, not a PDF, start here: Advertise with GolfN.

For how to run a rewards flight specifically, use How to Launch a Sponsored Rewards Campaign when that playbook is up.

Verify the audience before you scale the spend.

If the channel cannot tell you whether a golfer was real, everything downstream is a story. Stories are fine for brand films. They are a bad way to allocate a seven-figure sports budget.

The brands that win the next decade of golf will own relationships with people who play. Everyone else will keep renting eyeballs from people who watch.

Golf media buying is allocating budget across channels that reach golfers. Broadcast, digital, creators, apps, on-course, sponsorship-adjacent inventory. Done right, every dollar maps to an audience definition, a job, and a metric.

Most growth-oriented brands need a mix: verified first-party and in-app for performance, creators for culture and younger reach, search for intent, selective CTV and streaming for brand, and traditional golf media only when the target is older avid fans or prestige is the explicit KPI.

Yes, for the right job. Older, affluent, high-affinity audiences and brand presence. It is a weak primary channel if the goal is 18 to 34 players or measurable product action.

No universal split. A practical starting frame for growth brands is majority digital and first-party for performance, with sponsorship treated as brand storytelling that still connects to a measurable layer. Prestige-first brands invert that mix on purpose.

Where they spend time. Creators, social, apps, off-course venues. Not linear golf TV as the spine of the plan.

Social optimizes for platform engagement among people who might like golf. Verified golf apps optimize against people who play, often with activity confirmation and clearer post-click actions like offers and redemptions.

Use verified reach, engagement quality, and downstream actions. Not impressions alone. If a partner cannot report those, price the channel as brand theater.

As a verified-golfer, first-party environment for native placements, sponsored rewards, offers, and measurable engagement. Details and formats live on Advertise.

National Golf Foundation participation and rounds reporting as cited in GolfN's State of Golf Marketing 2026 and related Insights. Industry commentary on broadcast audience age and creator-led media from the same report and public trade coverage. Partner proof points (including Miura activation results) from GolfN partner programs. Always confirm the latest NGF release before updating annual numbers.

Jared Phillips is the CEO and co-founder of GolfN, the golf app that rewards you for playing. Before GolfN, he led sales and M&A in the insurance industry. He built GolfN because golfers create massive value for the sport and get almost nothing back. He writes about golf, rewards, and building products for people who actually play.

Sponsorship and advertising solve different problems in golf. A decision matrix for CMOs and partnership leads on what to buy, when, and how to measure it.

Step-by-step playbook for golf brands launching sponsored rewards campaigns: goals, prize design, targeting, creative, measurement, and common mistakes.

Decode golf media kits: what in-round, feed, sponsored rewards, offers, and sponsorship placements actually do, and when each is worth buying.