Insights9 min read

The Economics of Golf Loyalty & Rewards Programs for Brands

Brand-side economics of golf loyalty and rewards: who pays, what golfers do, unit economics, OEM and non-endemic use cases, and how to evaluate a partner.

![The State of Golf Marketing [2026]: Trends, Data & Opportunities](/_next/image?url=https%3A%2F%2Fcdn.sanity.io%2Fimages%2Fe3wja34v%2Fproduction%2Fc4d07e9bc51525c0f74f6cd6f2ee744dffdfc8bd-1200x630.png&w=3840&q=75)

Learn how GolfN can connect your brand with golf's most engaged audiences.

Explore Advertising →Golf is not having a moment. It is having a decade.

Eight consecutive years of on-course participation growth. 48.1 million Americans playing the game in some form. Record rounds. Record diversity. A demographic profile that would make most consumer brands rethink their entire media plan.

And yet most golf marketing still operates like it is 2015.

This is the first annual edition of our State of Golf Marketing report. It is designed to do one thing: give marketers, operators, and brands the clearest possible picture of who golfers are today, where their attention lives, and what it takes to reach them. Every number in this piece is sourced from primary data released in the last 12 months. If a stat is older, it is labeled as such.

The golf audience is bigger, younger, more diverse, and more valuable than the industry's marketing infrastructure reflects. That gap is the opportunity.

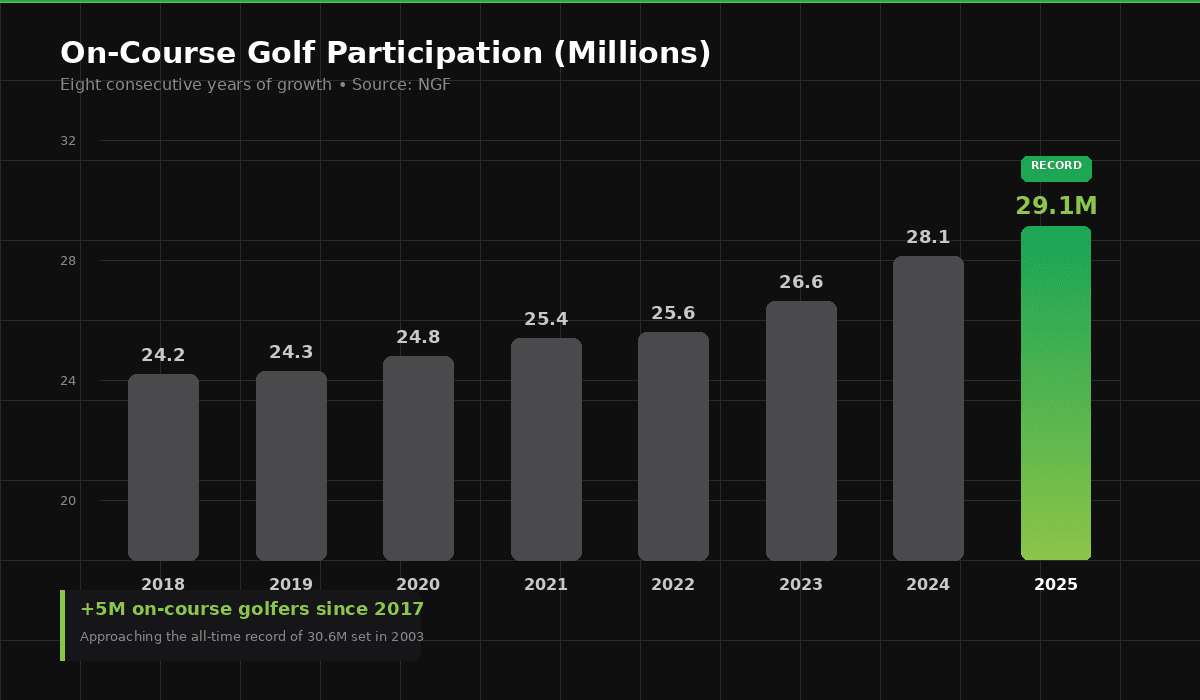

The National Golf Foundation's 2026 Graffis Report, released in January, confirmed what the data has been saying for years: this is not a COVID blip.

29.1 million Americans played golf on a course in 2025. That is the eighth straight year of growth and the highest on-course number since the Tiger Woods peak era of the early 2000s. Total participation, including off-course activities like entertainment venues and simulators, hit 48.1 million. Up 50% over the past decade. Up 41% since 2019. U.S. population grew 4.1% in the same window.

Rounds played hit another all-time record in 2025. The fourth record in five years. More than 550 million rounds at U.S. courses, running 21% above the five-year pre-pandemic average. And this happened with roughly 2,000 fewer courses than existed during the previous peak.

NGF CEO Greg Nathan has made a point worth repeating: the rise started in 2017, not 2020. The pandemic accelerated a trend that was already building. Participation growth, rounds growth, and demographic diversification were all underway before anyone had heard of social distancing. COVID gave golf a tailwind. The structural shift was already in motion.

Golf's total reach now extends to 136 million Americans. Two out of every five people in the country play, watch, read about, or follow golf in some form. The latent demand pool, non-golfers who tell the NGF they are "very interested" in playing, is 21 million deep and growing 37% since 2019.

The sport is not shrinking. It is accumulating.

Here is the number that should keep every golf marketer up at night.

Six million people played green-grass golf in 2025 who did not play in 2024. Net growth was one million. That means roughly five million people tried golf on a course and did not come back.

The NGF calls them "failed trials." The golf industry is exceptional at generating awareness and trial. It is not exceptional at converting trial into habit. Three million-plus beginners a year, four years running. And the net number barely moves.

This is the single biggest marketing problem in golf. Not awareness. Not reach. Retention.

Every dollar spent getting someone to try golf is wasted if there is no system to bring them back for round two, three, five, ten. The brands and operators who solve the retention loop will own the next era of golf growth. The ones who keep pouring money into top-of-funnel awareness without a re-engagement strategy are running on a treadmill.

The golfer your marketing is built for may not exist anymore.

The age flip. Adults aged 18 to 34 are now the largest cohort of on-course players in the United States, an estimated 6.3 million. Participation among this group has grown for six consecutive years. They now play more traditional golf than any other age group, according to LINKS Magazine and the NGF.

Traditional golf broadcast audiences still skew materially older. The median PGA Tour TV viewer has historically been over 60. The largest playing cohort is 18 to 34. The watching audience and the playing audience are different populations. Marketing plans built around broadcast golf alone miss the actual growth demographic entirely.

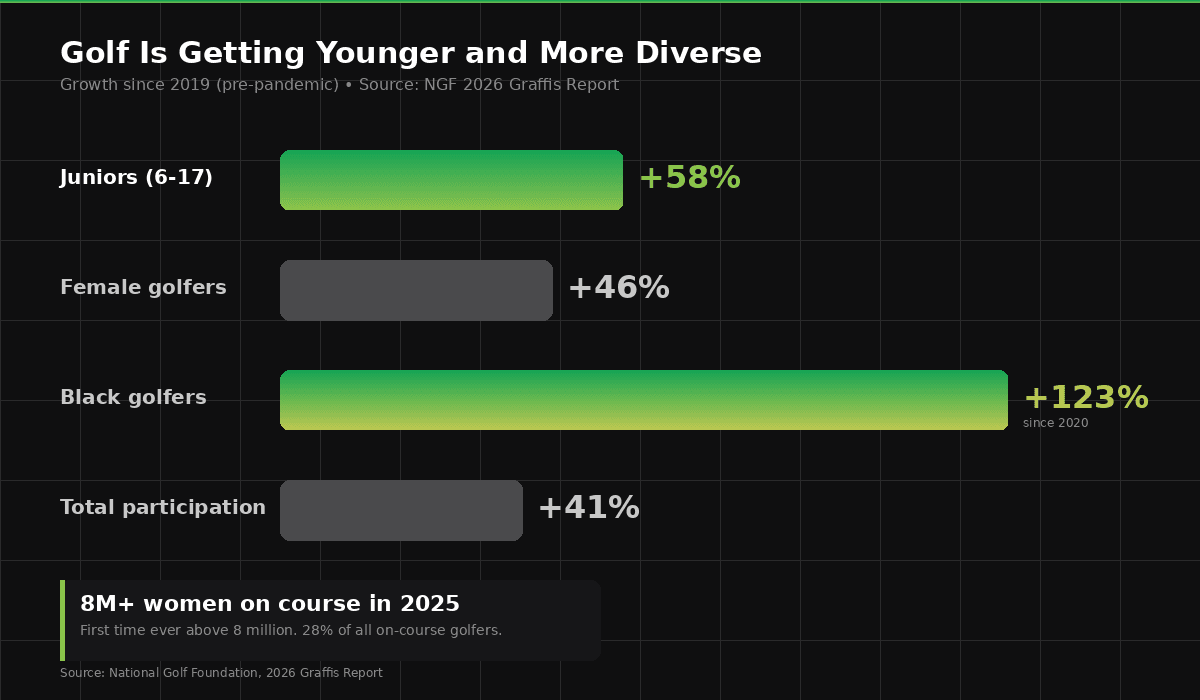

The diversity record. More than 8 million women and girls played on a course in 2025, the first time that number has ever crossed 8 million. Women now represent 28% of on-course golfers, matching the highest proportion on record. The net gain since 2019 is 2.5 million female golfers, a 46% increase. Women have accounted for roughly 60% of all net golfer growth since the pandemic.

People of Color on-course reached 7.7 million, another all-time high. That representation has moved from 8% in 1990, to 16% in 2000 during the Tiger effect, to over 25% today. Junior participation is up 58% since 2019, with 35% of junior golfers now being girls and 26% being People of Color.

The off-course participant pool is even more diverse. Among the 19 million Americans who exclusively play off-course golf, 43% are female and 45% are People of Color.

Why they play. This might be the most important shift of all. A Lightspeed survey of 700+ golfers found that 51% of Gen Z players rank mental health and self-care as their top reason to play golf. Not networking. Not business. Self-care. Among millennials, 53% cite time outdoors in nature as the leading motivator. Solo golf is rising fast: 76% of Gen Z golfers and 84% of millennials expressed interest in playing solo rounds.

Golf is being reframed as wellness, not business entertainment. Marketing that still positions golf as a networking tool is talking to a shrinking audience.

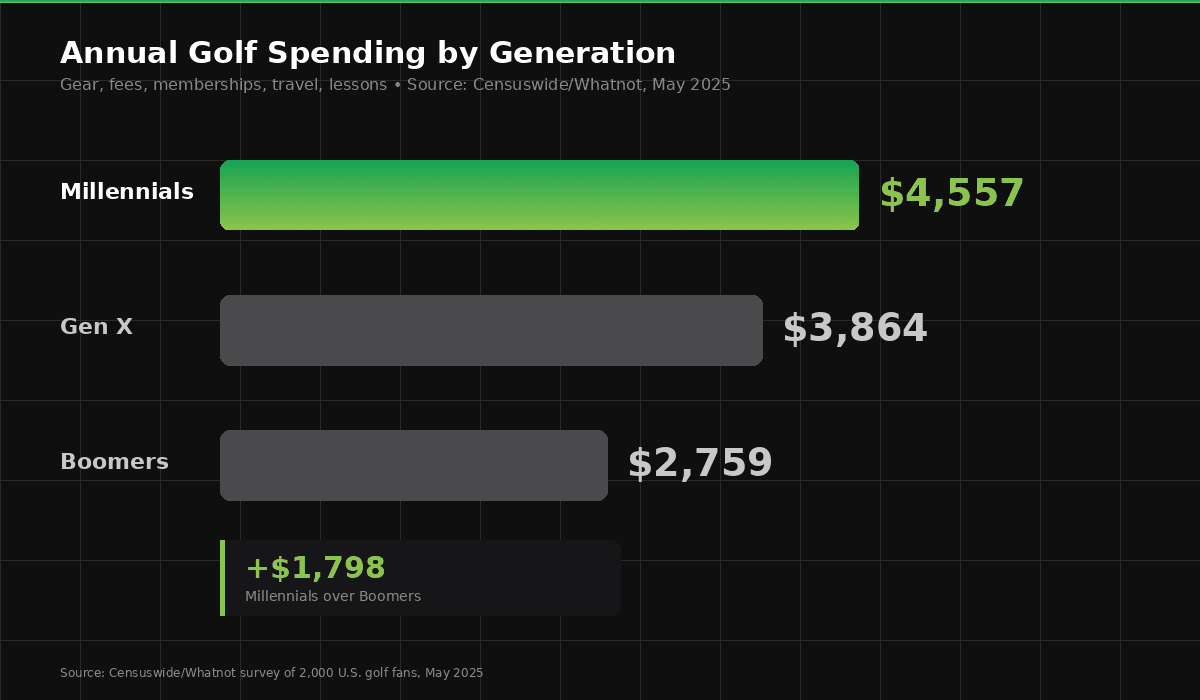

The spending power. Millennials expect to spend $4,557 per year on golf, according to a 2025 Censuswide and Whatnot survey of 2,000 U.S. golf fans. That is $693 more than Gen X and $1,798 more than Boomers. The idea that younger golfers are budget-constrained does not survive contact with the data.

Thirty-eight million Americans now play golf away from a traditional course. That includes entertainment venues, simulators, tech-enabled ranges, and practice facilities. Twenty-five years ago, the off-course number was under six million people hitting balls on driving ranges.

The golf simulator market alone is estimated at roughly $1.7 to $2.9 billion and growing at approximately 9 to 10% annually. But the more important story is behavioral, not financial. Simulators are normalizing year-round, weather-proof golf access and creating entirely new commercial touchpoints: sports bars, hotels, corporate offices, and urban entertainment venues where golfer relationships can be built.

Topgolf, with over 100 venues globally and $1.8 billion in segment revenue in 2024, demonstrated both the ceiling and the complexity of entertainment golf at scale. The planned spinoff from Callaway into a standalone public company, now likely in 2026, will be one of the most-watched moves in the golf business.

Here is the behavioral data that matters most. A Lightspeed survey found that 68% of Gen Z and 62% of millennials visit golf entertainment venues regularly. Fifty percent of Gen Z and millennials said they would consider replacing traditional golf outings with entertainment venue visits entirely.

Off-course golf is not a feeder system for traditional courses. For millions of people, it is the thing itself. Marketers who treat it as a lesser category are ignoring where the growth is.

When Gap launches a golf collaboration with Malbon and calls the campaign "Generation Golf," and Variety covers it, you are no longer looking at a sport. You are looking at a cultural surface.

Malbon Golf raised a $33 million Series B in 2025, hired a Nike veteran as CEO, and has expanded to the Philippines, China, Korea, and Vietnam. PGA Tour pro Jason Day left Nike for Malbon. The brand has collaborated with Adidas, New Balance, Jimmy Choo, and Coca-Cola. It is covered in fashion press and worn by Justin Bieber, Travis Scott, and Kevin Hart.

TravisMathew, part of Topgolf Callaway Brands, has built a billion-dollar-plus active lifestyle segment with ambassadors from comedy (Nate Bargatze) and the NFL (Jimmy Garoppolo). Korean golf fashion, what the industry calls K-golf, is rising globally.

The commercial implication is straightforward. Golf is no longer just a sport that marketers buy media around. It is becoming a lifestyle surface that marketers can build inside. Apparel, content, events, community, commerce. The brands that understand this convergence will reach golfers in places where golf-specific media never could.

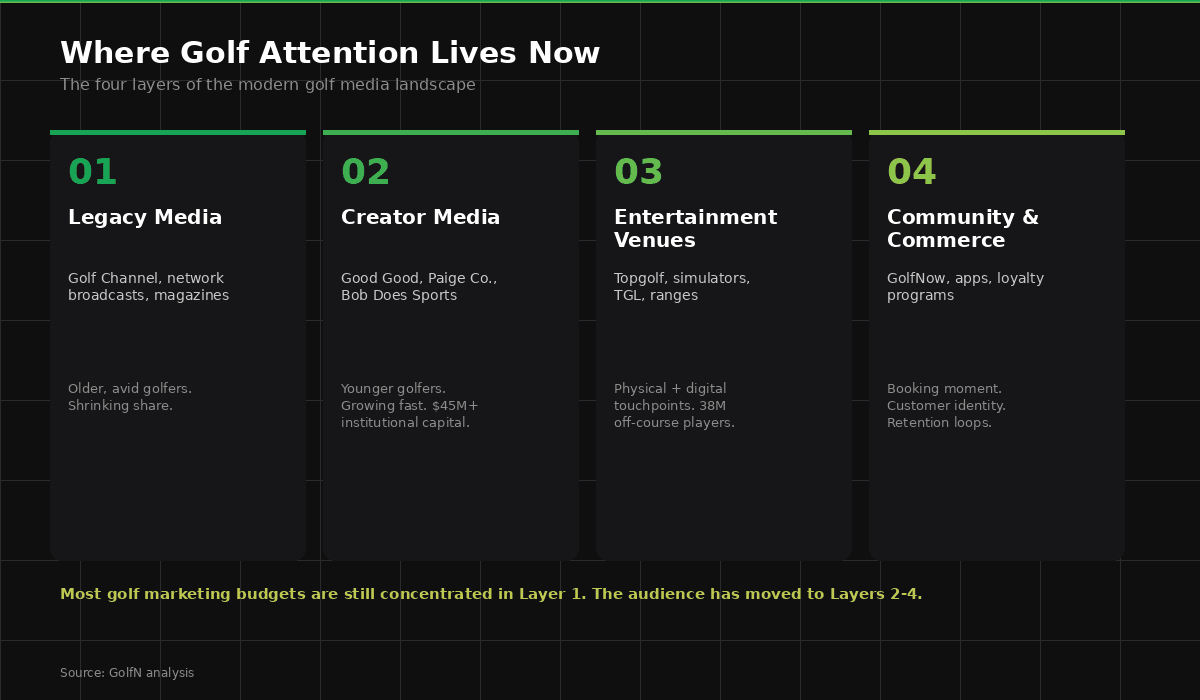

The golf media landscape has fundamentally changed. Most marketing budgets have not caught up.

Creator-led media is now institutional. In March 2025, Good Good Golf announced a $45 million funding round led by Creator Sports Capital, with participation from Manhattan West PE and Peyton Manning's Omaha Productions. Good Good has 1.75 million YouTube subscribers, co-branded Callaway gear sold at Dick's Sporting Goods, sold-out live events, and PGA Tour player sponsorships. They purchased an ownership stake in TGL's LA Golf Club. Their CEO has been transparent about the model: YouTube is the distribution vehicle, not the business. The business is golf commerce powered by creator community.

In February 2026, Paige Spiranac launched Paige Co. as a joint venture with Pro Shop, the golf media and commerce company behind Netflix's "Full Swing," Skratch, and GolfWRX. Spiranac, with over 11.6 million followers across platforms, is taking an equity stake and creative lead role. Pro Shop is handling production, distribution, sales, and merchandising. Their first project is a YouTube series.

These are not influencer deals. They are media companies with commerce infrastructure, creator-owned IP, event properties, and direct audience relationships. The capital markets are treating them that way.

The attention map has four layers now. Legacy golf media like Golf Channel, network broadcasts, and golf magazines still reach avid, older golfers. But their share of total golf attention is shrinking. Creator-led media (Good Good, Paige Co., Bob Does Sports, Rick Shiels) is where younger golfers actually spend time. Entertainment venues are physical attention environments that also generate digital touchpoints. And community and commerce platforms like GolfNow and various apps are where the booking moment and the customer relationship live.

Most golf marketing dollars are still concentrated in the first layer. The audience has already moved to the other three.

Nielsen's "Tops of Sports" report, released in December 2025, included a specific section on golf. PGA Tour viewership increased 10% in 2025 compared to 2024. Golf Channel live coverage was up 8% among total viewers. Two of four Majors and all three FedEx Cup Playoff events saw year-over-year increases.

The report explicitly notes that golf fans in the U.S. lean in with brand sponsors more than U.S. sports fans overall. With growing attention on the sport, Nielsen sees an opportunity for brands to connect with fans who are predisposed to support companies that sponsor the game.

TGL, the tech-infused indoor golf league backed by Tiger Woods and Rory McIlroy, is adding a new dimension. Nielsen's 2025 Global Sports Report found that 32% of TGL's 18-to-34 audience were not regular PGA Tour viewers. New format, new audience, new sponsorship inventory.

Golf's audience is affluent, brand-receptive, growing younger, and reachable across broadcast, streaming, creator content, live events, and apps. Most sponsors are still valuing golf on broadcast CPMs alone. The real value is in the full picture.

The first-party data opportunity in golf is enormous. But the strategic question is not just whether golf has rich data. It is who controls the touchpoints.

Course operators own the on-course experience but most lack digital infrastructure. Tee sheets, point-of-sale systems, and email lists are fragmented. Many courses still do not know who their golfers are in any actionable way.

Tee-time platforms are gaining control. GolfNow reported seven of its top 10 booking days in company history during the first nine months of 2025, broke all-time monthly records for total rounds booked five times, and set more than 55 all-time records through September. The platform serves 3.5 million registered golfers and has expanded beyond tee times into simulator bookings and pro-shop merchandise pre-orders. Internationally, new GolfNow bookers increased 50% year-over-year in the UK and Ireland.

OEMs have strong brand relationships but limited post-purchase behavioral data. Callaway/Topgolf has the most integrated position: venues, equipment, lifestyle brands, and Toptracer data all under one umbrella.

Entertainment venues capture visit-level behavioral data but typically do not follow the golfer outside the venue.

Creator brands like Good Good and Paige Co. own attention and community and increasingly own commerce. They do not yet own playing-moment data.

Apps and loyalty programs are the contested space. Whoever builds the authenticated identity layer that connects playing behavior, purchasing behavior, and content consumption wins the data game.

The golfer relationship is currently fragmented across five or six parties, none of whom see the full picture. The biggest opportunity in golf marketing is building the connective tissue that links who golfers are, how they play, what they buy, and what content they engage with. The booking moment is a critical control point. The playing moment is still largely uncaptured digitally for most golfers.

Google reversed its plan to fully deprecate third-party cookies in Chrome. As of April 2025, Chrome keeps them enabled by default. Users can toggle the setting, but most do not.

This does not mean the old targeting world is back. Safari and Firefox already block third-party cookies by default. Chrome holds roughly 67% of global browser share. Privacy pressure, browser fragmentation, and marketer behavior have already pushed the market toward direct data and consented relationships. Only 49% of brands now say cookies are essential to their strategy, down from 75% in 2022, according to Adobe. Ninety percent of marketers report shifting their personalization tactics and data mix, per the IAB. Only 15% of global marketers told Deloitte they felt fully prepared for a cookieless world.

The trajectory is irreversible regardless of what Chrome does.

Golf generates uniquely valuable first-party data. Round-by-round behavior. Scoring patterns. Equipment preferences. Course preferences. Spending habits. Location data. Forty-eight million participants with touchpoints across apps, tee-time bookings, pro shops, entertainment venues, and simulators. A total reach of 136 million.

The industry is sitting on this data while most golf marketing still runs on spray-and-pray media buys and generic sponsorship placements. First-party behavioral data can improve customer acquisition costs by 83% and boost ROI by 72%, according to Adtelligent.

The retention gap makes this urgent. Six million new trials, one million net growth. The gap closes when you build re-engagement loops powered by direct data: personalized post-round offers, automated onboarding sequences for beginners, dynamic pricing tied to behavioral patterns. AI is the layer that scales this from a nice idea to an operational reality.

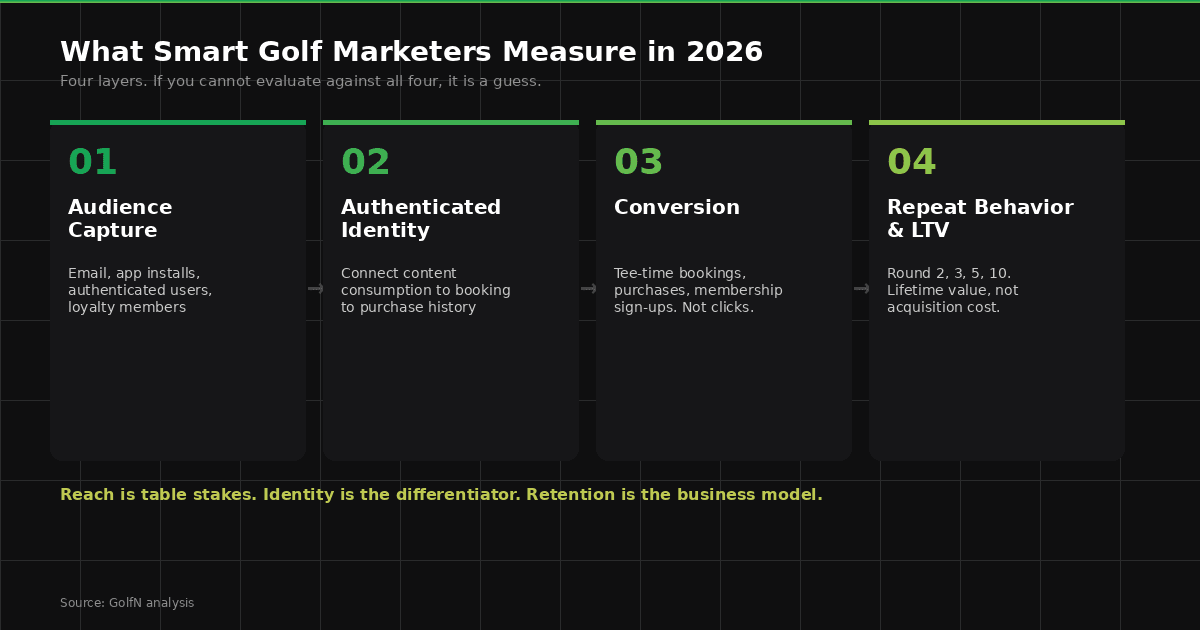

Most golf marketing is still measured in impressions and reach. Those metrics tell you how many eyeballs you theoretically accessed. They do not tell you whether anyone cared, bought, or came back.

Modern golf marketing should be evaluated across four layers.

Audience capture. Are you building a first-party audience you own? Email, app installs, authenticated users, loyalty program members. If your marketing drives awareness but does not capture identity, you are renting attention.

Authenticated identity. Do you know who your golfers are across touchpoints? Can you connect their content consumption to their booking behavior to their purchase history? This is the connective tissue that most golf marketing lacks.

Conversion. Are you driving measurable actions? Tee-time bookings, equipment purchases, membership sign-ups, event registrations. Not clicks. Not impressions. Transactions.

Repeat behavior and lifetime value. This is where the retention gap becomes a measurement problem. Are your marketing efforts bringing golfers back for round two, three, five, ten? Lifetime value is the metric that separates golf marketers who build lasting businesses from those who burn budget.

Any golf marketing investment that cannot be evaluated against these four layers is a guess, not a strategy.

Golf in 2026 is not the sport it was in 2019. The participants are different. The motivations are different. The entry points are different. The media landscape is different. The data infrastructure is different.

The marketers, brands, and operators who recognize this will build relationships with the most valuable consumer audience in American sports. The ones who do not will keep marketing to an audience that is getting smaller every year.

48.1 million participants. 136 million in total reach. Record rounds on fewer courses. A younger, more diverse, higher-spending audience that plays for self-care and consumes golf through creators, not cable.

The data is not ambiguous. The opportunity is not theoretical. The question is execution.

This is the first annual edition of GolfN's State of Golf Marketing report. It will be updated and republished annually as new data becomes available. If you found this useful, share it with someone who makes decisions about how golf marketing dollars get spent.

Sources cited in this report include: National Golf Foundation (2026 Graffis Report, 2025 Graffis Report, Golf Industry Facts, CEO year-end letter); USGA (2025 National Scorecard); Nielsen ("Tops of Sports" Dec 2025, 2025 Global Sports Report); Lightspeed Commerce (2025 Golf Industry Trends survey, 700+ golfers); Censuswide/Whatnot (2,000 U.S. golf fans, May 2025); Topgolf Callaway Brands (SEC filings, earnings releases); GolfNow (press releases via The Golf Wire, NBC Sports); Good Good Golf (Business Wire, March 2025); Axios (Paige Co./Pro Shop, Feb 2026); Gap Inc. (Malbon collaboration press release); Puck (Malbon Golf Series B); Adobe, IAB, Deloitte, Adtelligent (marketer readiness and first-party data research); Grand View Research, Fortune Business Insights (simulator market data).

Jared Phillips is the CEO and co-founder of GolfN, the golf app that rewards you for playing. Before GolfN, he led sales and M&A in the insurance industry. He built GolfN because golfers create massive value for the sport and get almost nothing back. He writes about golf, rewards, and building products for people who actually play.

Brand-side economics of golf loyalty and rewards: who pays, what golfers do, unit economics, OEM and non-endemic use cases, and how to evaluate a partner.

Sponsorship and advertising solve different problems in golf. A decision matrix for CMOs and partnership leads on what to buy, when, and how to measure it.

Step-by-step playbook for golf brands launching sponsored rewards campaigns: goals, prize design, targeting, creative, measurement, and common mistakes.